GROSS PAY, PAYROLL DEDUCTIONS & NET PAY

Taken from:

http://www.monster.ca/career-advice/article/understand-your-canadian-pay-slip

The Pluses

The amount under or next to “Total Earnings” holds top rank for being the biggest dollar value on your pay slip. It combines your gross income and your taxable benefits such as RRSP top-up payments made by your employer, or taxable allowances like travel per diems, car and cell phone payments or any perk you write off on your expense report that is paid or reimbursed to you by the company. Your premiums and tax rate is determined by your total insurable earnings.

The amount under or next to “Gross Income” is the second highest amount on your pay slip. It’s the amount of your regular salary, wages, commissions or earnings before deductions.

The Minuses

“Net Pay” is the diminutive baby bear, the third largest number on your pay stub and several hundred dollars lower than your gross income and total insurable earnings. This is the amount of salary left over once all the deductions are removed.

Here’s where your money went:

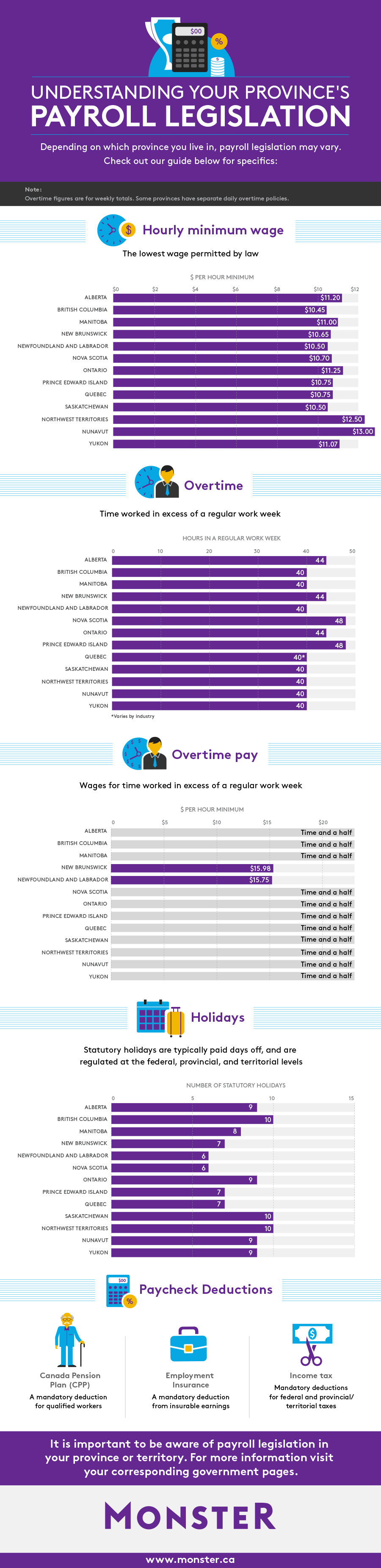

1. Government Pension is the number one line item under the deductions subheading. This refers to your mandatory Canada Pension Plan (CPP) contribution.

*Quebecers pay into the QPP. The other Quebec exception is the Quebec Parental Insurance Plan (QPIP) premium. Revenue Quebec provides online access to a source deductions calculation program to help employers figure out these amounts.

2. Employment Insurance (EI) is the next premium that gets deducted from your salary. Your premium payment will be $1.73 for every $100 of insurable earnings until you pay out the maximum contribution amount of $747.36. Quebec residents pay $1.36 per $100 of insurable earnings up to $587.52.

3. Following CPP and EI is federal and provincial income tax. You file a TD1 form when you start your job, telling both levels of government what you can claim as tax credits. The TD1 data is used to determine your tax deduction rate.

4. Finally, you have non-compulsory deductions. If you pay child support directly out of your paycheck you’ll incur it as a minus. If you pay group insurance premiums these contributions will show up on your pay stub on a separate line. These premiums will vary between companies based on the plan purchased and the employer contribution. You might also see your RRSP deductions if you pay into your company RRSP matching plan.

Keep in mind you can keep track of all the deductions by pay period or lumped into a sum by looking at the Year To Date column (YTD).

It’s your responsibility to understand your deductions and monitor your pay so that in the event of a calculation error by the employer you can catch it and have it rectified pronto.

If you have any questions about your pay slip see or speak with your manager, company payroll specialist or contact the Canada Revenue Agency.

http://www.monster.ca/career-advice/article/understand-your-canadian-pay-slip

The Pluses

The amount under or next to “Total Earnings” holds top rank for being the biggest dollar value on your pay slip. It combines your gross income and your taxable benefits such as RRSP top-up payments made by your employer, or taxable allowances like travel per diems, car and cell phone payments or any perk you write off on your expense report that is paid or reimbursed to you by the company. Your premiums and tax rate is determined by your total insurable earnings.

The amount under or next to “Gross Income” is the second highest amount on your pay slip. It’s the amount of your regular salary, wages, commissions or earnings before deductions.

The Minuses

“Net Pay” is the diminutive baby bear, the third largest number on your pay stub and several hundred dollars lower than your gross income and total insurable earnings. This is the amount of salary left over once all the deductions are removed.

Here’s where your money went:

1. Government Pension is the number one line item under the deductions subheading. This refers to your mandatory Canada Pension Plan (CPP) contribution.

*Quebecers pay into the QPP. The other Quebec exception is the Quebec Parental Insurance Plan (QPIP) premium. Revenue Quebec provides online access to a source deductions calculation program to help employers figure out these amounts.

2. Employment Insurance (EI) is the next premium that gets deducted from your salary. Your premium payment will be $1.73 for every $100 of insurable earnings until you pay out the maximum contribution amount of $747.36. Quebec residents pay $1.36 per $100 of insurable earnings up to $587.52.

3. Following CPP and EI is federal and provincial income tax. You file a TD1 form when you start your job, telling both levels of government what you can claim as tax credits. The TD1 data is used to determine your tax deduction rate.

4. Finally, you have non-compulsory deductions. If you pay child support directly out of your paycheck you’ll incur it as a minus. If you pay group insurance premiums these contributions will show up on your pay stub on a separate line. These premiums will vary between companies based on the plan purchased and the employer contribution. You might also see your RRSP deductions if you pay into your company RRSP matching plan.

Keep in mind you can keep track of all the deductions by pay period or lumped into a sum by looking at the Year To Date column (YTD).

It’s your responsibility to understand your deductions and monitor your pay so that in the event of a calculation error by the employer you can catch it and have it rectified pronto.

If you have any questions about your pay slip see or speak with your manager, company payroll specialist or contact the Canada Revenue Agency.